Market volatility balances itself out; prices are about where they were a year ago

The small decline in the Department of Energy/Energy Information Administration diesel price this week is notable mostly when a look into the past is undertaken.

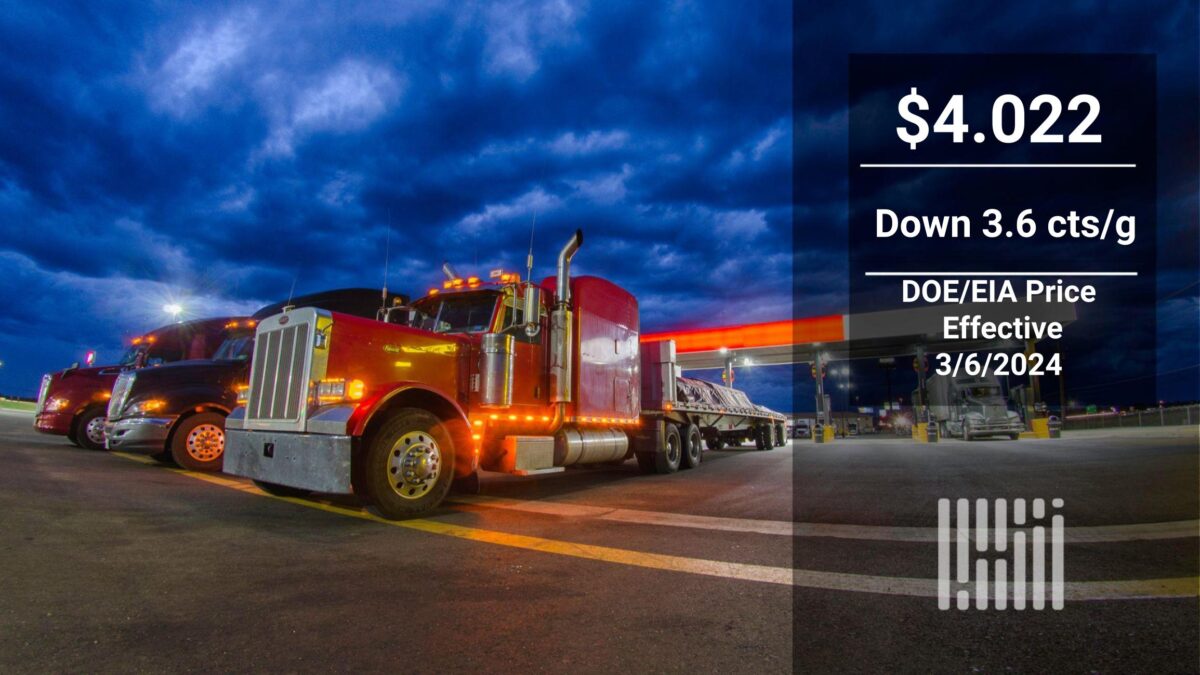

The price published by DOE/EIA that is used for most diesel surcharges was $4.022 per gallon effective Monday, a drop of 3.6 cents a gallon from a week earlier. In the last three weeks, the price has been unchanged, down 5.1 cents a gallon and then followed by this week’s decline.

Fifty-two weeks ago, on March 6, 2023, the DOE/EIA price was $4.282 cents a gallon, 26 cents more than Monday’s price.

But Monday also was the time for another comparison: the price of crude now versus a year ago.

On March 6, 2023, West Texas Intermediate (WTI) settled at $80.46 a barrel, though the price of WTI just prior to that data had been holding relatively firm at levels less than $80 a barrel.

A year later on Monday, the WTI settlement was $78.74 a barrel. That means that over 12 months, against a background of OPEC+ implementing significant cuts in output — when U.S. production soared more than 1 million barrels a day to 13.3 million barrels a day, and when countries like Guyana and Brazil saw their own output climb as well — the only thing that happened is that the price of the U.S. benchmark crude declined about 2.2%.

Brent, the international crude benchmark, settled Monday at $82.80 a barrel, a drop of 4% over the last 52 weeks.

But the retail price of diesel as measured by the DOE/EIA price was down 6% after posting this week’s number.

This is good news for diesel consumers because the diesel market expressed as a spread against crude has, for several years now, been significantly higher than historic norms. And when that situation prevails in the commodity market, it eventually makes its way down to the pump, with retail diesel unable to take advantage of all the decline posted in the crude market.

Comparing the price of Brent and ultra low sulfur diesel on the CME commodity exchange Monday produces a spread of about 67.5 cents a gallon. A year ago, that spread was about 83.5 cents a gallon. The narrowing of that spread back toward more historic norms is one of the reasons why the retail price of diesel has fallen more in the past 52 weeks than what the price of crude has done.

There is no single reason why that spread has narrowed. A year ago, the market was coping with uncertainty over Russian supplies of diesel one year after the invasion of Ukraine. Those supplies have mostly returned to normal.

A bullish factor is that inventories are tighter than a year ago, as indicated by the 12-month spread on the forward curve for ULSD on CME.

A year ago, about 4.75 cents a gallon separated the first month ULSD contract from the contract 12 months out. When the front month is higher than the out months, it is a structure called backwardation, and it occurs when inventories are tight and the most sought-after barrel in the market is the one that can be delivered the quickest.

But the 12-month backwardation Monday was about 20.4 cents a gallon, suggesting tighter inventories worldwide. And yet the spread between crude and diesel has softened during the last year.

Supply of refining capacity has been bearish for diesel. There has been new refining capacity that has come online worldwide, most notably the giant Dangote refinery in Nigeria. But closer to home, just about a year ago, ExxonMobil (NYSE: XOM) brought on 250,000 barrels a day of new refining capacity at its refinery in Beaumont, Texas, which also may be contributing to softer diesel margins.

Renewable diesel (RD) capacity is rising in the U.S. as well. And while some new renewable diesel projects are occurring at former integrated refineries that have closed, with the end result being that the renewable diesel quantities being produced are not offsetting the conventional diesel output lost, the fact is that those closures were often several years ago and the new RD capacity has been coming online now, with more growth to come this year.

Put those factors together and you get a situation where while the ride has been wild, the reality is that the crude market is pretty much now about where it was a year ago. That can’t really be said about diesel.